Falsifying business records.

Issuing false financial statements.

Sound familiar?

If you follow the Donald Trump court cases piling up from sea to shining sea, you know that this is a reference to the ex-president’s civil fraud case where a judge ordered him to pay the State of New York $355 million in penalties.

But it also applies to something a lot closer to home.

And a lot closer to middle class America than Wall Street.

Remember the mortgage crisis?

The housing meltdown?

The Great Recession?

All three have been in the rearview mirror for roughly a dozen years.

They shouldn’t be too hard to remember.

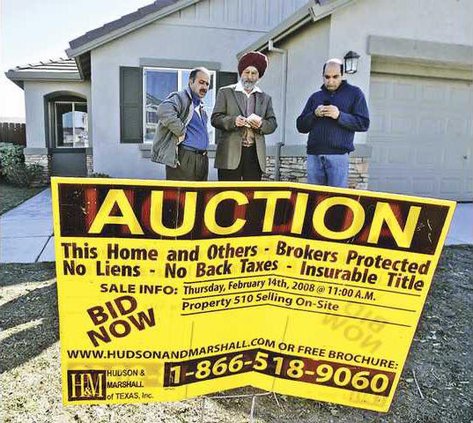

San Joaquin County was ground zero for foreclosures.

Stockton, Manteca, Lathrop, Mountain House, and Tracy being the biggest hit.

Manteca at one point had more than 400 homes in the foreclosure process at the same time.

In excess of 1,200 homes in Manteca eventually got caught up in the mess.

Most went into foreclosure and were repossessed.

Some of those went to auction.

The rest were marketed at fire sale prices by banks.

There were a sizable number of short sales.

And there were a rare few that the buyers caught up and became current.

In 2012, Stockton became the largest city at the time to file bankruptcy.

And much of the problem was attributed to “liar loans.”

“Liar loans” is a reference to the overstating the annual pay of borrowers applying for mortgages.

It also referenced the self-employed that secured loans by the overstatement of the value of their assets.

There were unscrupulous loan originators involved.

There were banks that didn’t do their due diligence or knowingly looked the other way.

And they were those that packaged mortgages on the secondary resale market who knew what get were doing was toxic.

Big business conducting fraud on Americans, right?

Not exactly.

There were few documented cases of signed loan documents or income verification forms being altered after the person seeking a mortgage signed them.

A majority of loans at one point had inflated income on the documents borrowers signed.

In some cases, there were arguments language barriers were involved.

But overall there is no justification for what borrowers did.

Buying a home is the biggest expenditure most Americans will ever make.

Given the process securing a loan and buying a home involves, one clearly has an idea of their income.

Unless, of course, they falsified 1040 forms, which is another criminal issue, or provided fraudulent paycheck stubs.

The most critical part of the loan document is income.

It is a stretch that makes Silly Putty seem like concrete that those borrowers reading and signing loan documents were clueless to their income when they are buying a home.

And it wasn’t a victimless crime.

Foreclosures spurred neighborhood blight and community crime.

And they triggered the deepest economic downturn that affected everyone -— renters and homeowners alike — since the Great Depression.

A lot of people who benefitted — and subsequently got burned by liar loans and at the same time partially burning down the economy — are still around these parts.

All of this prompts the question: Should those that lived in houses of glass thanks to deceptive means be screaming to tar and feather someone who did essentially what they did?

Do not misunderstand.

This is neither in defense or in commendation of Trump.

There are also a lot of other issues in other courts in play besides the civil fraud trial.

Overstating income or assets to attain a real estate loan brings the full prosecutorial force of the office of New York State Attorney General Letitia James down on you.

There are countless San Joaquin County residents that are lucky James was not this state’s attorney general 12 to 16 years ago.

The same for having a New York style law on the books that makes it civil fraud to overstate assets to secure loan.

Trump court cases, in terms of public reaction, follow a pattern.

Both sides — in the courtroom and in politics — are painting everything in black and white.

And in some cases that is the case.

But when it comes to Trump’s civil fraud trial we all need to check our moral compasses.

They seem to have been taken over by the blood sport pull of partisan politics.

Lying is lying.

But situational ethics based on political narratives aren’t any better.

There may indeed be enough to legally sink Trump in a manner that channels justice and doesn’t reek of retribution.

The civil fraud case — and how the law is applied and against who it is applied — is another issue.

That doesn’t excuse Trump or anyone from what the court determined.

It doesn’t matter that there was no evidence of lenders being harmed.

The system was gamed. And under New York law, gaming the system in such a manner is civil fraud.

But there is an asterisk.

It is only prosecuted by the State of New York if AG James determines it is fraud.

Her office is intervening on the behalf of the American Irish Historical Society in a dispute where they significantly overvalued the value of their building.

If overvaluing assets to attain a loan constitutes civil fraud and is illegal, one would expect those in charge of the legal system be consistent in applying the law.

Whether Joe Biden or Donald Trump should be President is a matter for the court of public opinion.

Cheering or even condemning what has happened in New York should have us all looking in the mirror.

We are in danger of losing our sense of justice and fairness in this country.

The ends should never justify the means when those means are less than honorable.

And that is whether one thinks Trump walks on water or is Lucifer’s twin.

Getting someone elected or defeated at all costs undermines the high ground.

That needs to be kept in mind as the 2024 president race slithers to Nov. 5.

The biggest threat to democracy is when we lose our moral bearings in a myopic bid to get whoever we as individuals believe should be in office elected.

This column is the opinion of editor, Dennis Wyatt, and does not necessarily represent the opinions of The Bulletin or 209 Multimedia. He can be reached at dwyatt@mantecabulletin.com